With around 11,000 currently operating worldwide, data centres are not a new phenomenon, but recent growth in the number and sheer scale of new data centres is dramatically changing the market. A combination of accelerated global digitalisation, cloud adoption and, of course, the fast-growing use of generative artificial intelligence (GenAI) is driving this extraordinary growth in demand for computing power.

The Gulf region is playing a major role in this development, with ambitious plans from GCC governments, backed by investment, to transform it into a digital hub. Government initiatives such as Saudi Vision 2030 and UAE Centennial 2071[1] that promote the strategic pursuit of smart cities, e-governance, AI and cloud services, are driving the development of further digital infrastructure as the GCC invests to consolidate its collective vision as a global digital powerhouse. With its strategic location straddling several important subsea data cables connecting Europe, Asia and Africa[2], and the availability of reliable, low-latency fibre-optic connectivity, as well as abundant and cheap renewable solar energy, the region is attracting an increasing number of data centres.

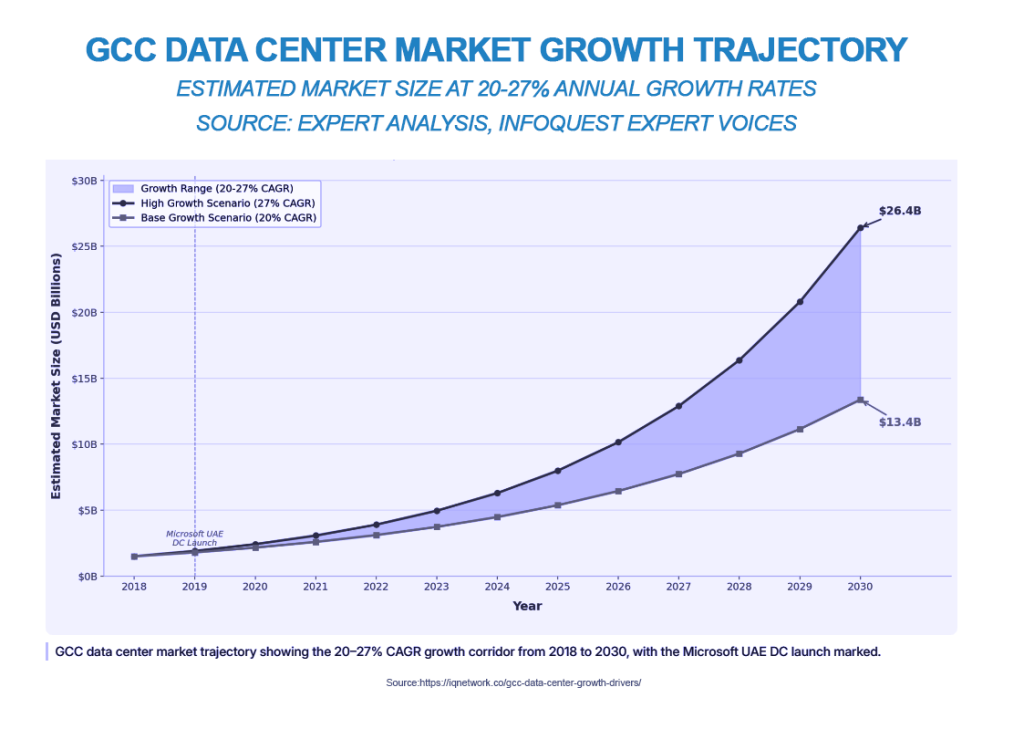

As digitalisation, cloud adoption and AI grow rapidly, various GCC governments have issued clear, new regulations to govern cloud sovereignty and data localisation in their respective jurisdictions, giving the Gulf’s data-centre market an unprecedented boost. Government regulations now require public-sector data, as well as other sensitive data, to be hosted nationally, creating a regulatory environment that requires international data-centre operators to develop physical infrastructure in the GCC to satisfy data-residency mandates[3]. As a result, the GCC’s data-centre market is expected to exceed US$ 9 billion by 2030, up from just US$ 3.5 billion two years ago.[4]

GCC data centres: where is the insurable risk?

The growing opportunities for re-insurers were underlined recently by Guy Carpenter’s CEO, when he described data centres as “the single biggest new business opportunity in 2026”.[5]

Global annual investment is likely to reach US$300 billion by 2027, according to S&P Global,[6] with Marsh suggesting that investment could exceed US$3 trillion within five years.[7] This rapid growth is therefore opening up new opportunities for re-insurers, with the chance to expand and deepen their offerings for new enterprise, cloud and hyperscale AI data-centre projects where insured values of between US$10 billion[8] and US$30 billion for construction alone are not uncommon.

The sector is currently well supported by the re-insurance industry, with players such as Aon already more than doubling capacity for coverage,[9] but further scaling of coverage will be needed to support growth in this sector.

Property and business interruption risk form a large part of the growing opportunities for re-insurers in the region, given the expectation that Tier 4 data centres – the most fault-tolerant of all[10] – will achieve 99.995% of uptime annually. Fire risk, cyber-attacks, and natural catastrophes also feature heavily in the risk profile of new data centres, as does the reliability of primary and back-up power and water supplies for cooling, which are critical to uninterrupted operations.

Well-established enterprise and cloud data centres offer some loss history for pricing risk, but new hyperscale AI projects present an entirely new set of risks and opportunities, given the immaturity of the market and the scarcity of loss history or claims data, making the job of pricing risk something of an evolving science.

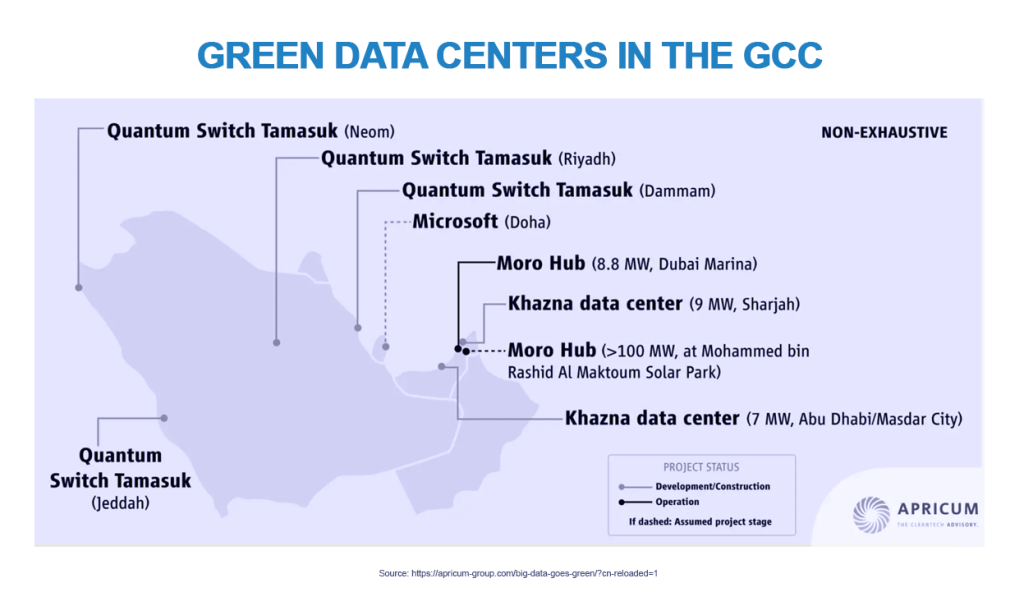

As we discuss in greater detail below, the requirements in the GCC for sustainability in the development of new data centres add another layer of insurable risk, in the form of proprietary renewable-energy generation. In Saudi Arabia, for example, a new 1.5 GW data-centre campus for high-density AI demands in Oxagon, NEOM’s new industrial city on the Red Sea coast, will be powered exclusively by Oxagon’s solar energy, wind energy and green hydrogen[11][12] installations. In Dubai’s Mohammed bin Rashid Solar Park, the 100 MW Moro Hub is the world’s largest data centre to run exclusively on solar energy[13].

According to Hiscox Power & Renewables underwriter, Louis Cozon, “the renewable projects needed to meet this power demand will only go ahead if they are supported by the insurance industry. The market needs to continue to sustainably provide products protecting power facilities and their investors from a wide range of risks”.[14]

The JENOA view: Why is the GCC such an attractive location for new hyperscale data centres?

Owing to their significant electrical and cooling requirements, data centres are power-hungry and resource-hungry installations, and the International Energy Agency estimates that in 2024, they consumed 1.5% of the global power supply.[15] With exponential growth in demand for AI computing power anticipated, that figure is likely to double to nearly 1,000 terawatt hours (TWh) by 2030, which is more than the total annual electricity consumption of Japan.[16]

The GCC, however, is well-positioned to gain a significant competitive advantage over other host nations in accessing the more affordable and sustainable resources that data centres will need to operate successfully. For the GCC, large-scale development from scratch coincides with the growing availability of cheaper, more reliable sources of sustainable energy, but also takes advantage of the fact that reliable solar resources are a natural feature of the GCC’s geographical location. This offers a substantial cost advantage, with energy costs around 30%–50% below global averages.[17] When combined with an abundance of state-owned land in nations such as the UAE and Saudi Arabia, co-locating data centres and energy generation becomes easier, and permitting can be smoother, without the complications and delays inherent in private land-ownership negotiations elsewhere. Such strategic co-location of power generation alongside new data centres would also remove the need to find and negotiate power purchase agreements (PPAs) on a global scale in order meet clean-energy targets. Microsoft, for example, in partnership with Fotowatio Renewable Ventures (FRV) and others, has already contracted 40GW of generation to meet its 2025 target of 100% renewable energy.

Sustainability certifications such as the UAE’s “Estimada” have become an integral part of design and planning for data-centre construction and permitting, and as various jurisdictions in the GCC begin to encourage or mandate the sustainable use of resources for new projects, the opportunity for the GCC to outperform other nations in the sustainable construction and operation of new data centres is significant. After all, when the requirement for sustainable practices is baked into a project’s design and planning phases, operators can achieve a more efficient, more environmentally friendly and more cost-effective project than is possible when retrofitting existing sites.

Power consumption is not the only consideration when it comes to sustainability; data centres typically require pumping vast quantities of water through systems such as the widely used evaporative room-cooling method[18] to cool server stacks operating at high temperatures. The Gulf’s climate puts yet more pressure on the need for cooling, and although the use of desalination plants in the region is widespread, desalinated water is energy intensive.

Alternative technologies for cooling, however, are making the GCC an attractive location for new data centres as local operators begin to adopt more water-efficient cooling methods. Immersion, seawater cooling, air- and liquid-cooling systems, and full-scale cooling are emerging as viable alternatives, along with so-called adiabatic free-cooling chillers, which minimise the need for water evaporation and vastly improve efficiency,[19] thus helping to preserve potable water supplies.

What does this mean for MENA clients – and how can JENOA help?

With access to global re-insurance markets including Lloyds of London, JENOA’s strong focus on data-driven insights allows us to help clients perform more in-depth risk-exposure analysis in emerging risk landscapes to manage risk more effectively.

JENOA is well placed to help clients source adequate regional and international re-insurance capacity for growing data-centre needs. Our experience in tailored solutions for energy-related investments makes us an invaluable partner in helping clients innovate and develop new products.

Expanding and deepening capacity: can re-insurers meet the GCC’s growth in data centres?

As the GCC emerges as a global frontrunner in data-centre construction and operation, the opportunities to innovate in specialised construction, operational and energy risk are likely to grow exponentially, giving re-insurers in the region an unprecedented boost in insurable risk.

Supported by national visions that cement the GCC as a truly global and sustainable digital powerhouse, the region attracts an increasing number of operators keen to take advantage of its favourable environment, digital infrastructure, and position as a premier location for development at a crucial digital intersection between Africa, Asia, and Europe.

1] https://beam.ai/agentic-insights/the-better-future-is-coming-with-uae-vision-2071

[2] https://www.trtworld.com/article/ed01b7fdc9c3

[3] https://www.addleshawgoddard.com/en/insights/insights-briefings/2025/real-estate/future-data-centres-gulf-cooperation-council/

[4] https://www.researchandmarkets.com/report/middle-east-data-centers-market

[5] https://www.reinsurancene.ws/data-centres-present-the-single-biggest-new-business-opportunity-in-2026-marsh-execs/

[6] https://www.spglobal.com/ratings/en/regulatory/article/data-centers-offer-a-hyperscale-pool-of-insurable-risks-s101669146

[7] https://www.reinsurancene.ws/data-centres-present-the-single-biggest-new-business-opportunity-in-2026-marsh-execs/

[8] https://www.businessinsurance.com/insurers-brokers-react-to-data-center-boom/

[9] https://www.businessinsurance.com/insurers-brokers-react-to-data-center-boom/

[10] https://www.hpe.com/uk/en/what-is/data-center-tiers.html

[11] https://www.linkedin.com/pulse/rise-digital-gulf-data-center-growth-gcc-geneire-international-zlvdf/

[12] https://www.datacenterdynamics.com/en/news/datavolt-plans-15gw-data-center-campus-in-neoms-oxagon/

[13] https://www.linkedin.com/pulse/rise-digital-gulf-data-center-growth-gcc-geneire-international-zlvdf/

[14] https://www.hiscoxlondonmarket.com/blog/how-insurance-industry-critical-data-centre-revolution

[15] https://www.iea.org/reports/energy-and-ai/energy-demand-from-ai

[16] https://www.hiscoxlondonmarket.com/blog/how-insurance-industry-critical-data-centre-revolution

[17] ttps://www.addleshawgoddard.com/en/insights/insights-briefings/2025/real-estate/future-data-centres-gulf-cooperation-council/

[18] https://www.lincolninst.edu/publications/land-lines-magazine/articles/land-water-impacts-data-centers/

[19] https://gowlingwlg.com/en-gb/insights-resources/articles/2025/building-and-powering-data-centres-in-the-gcc