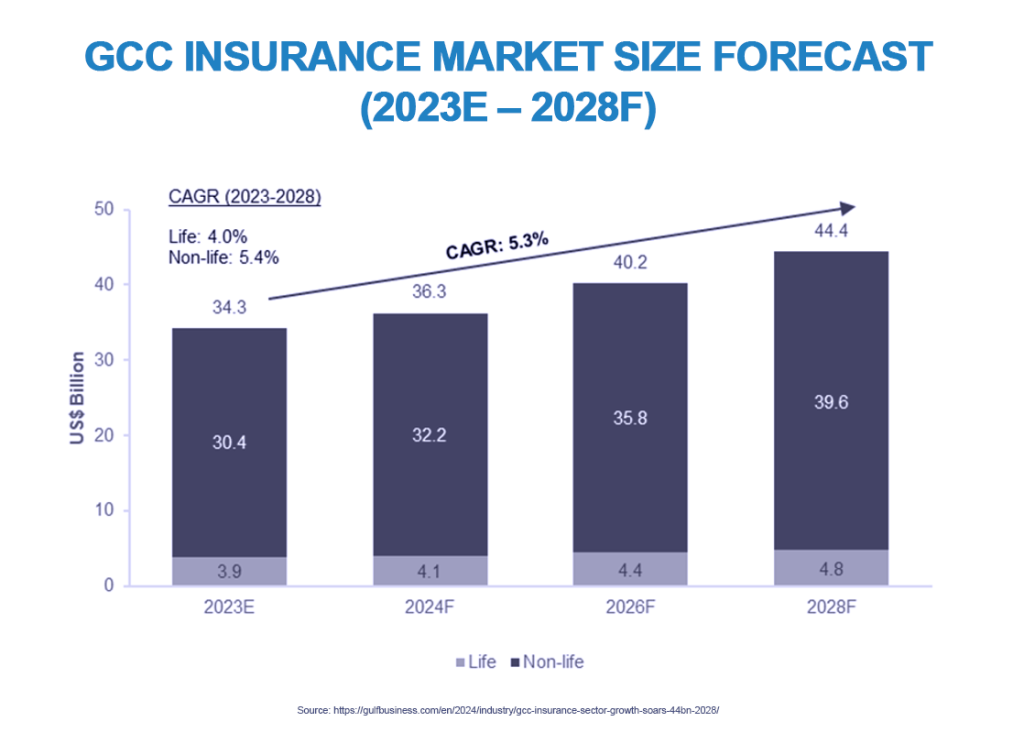

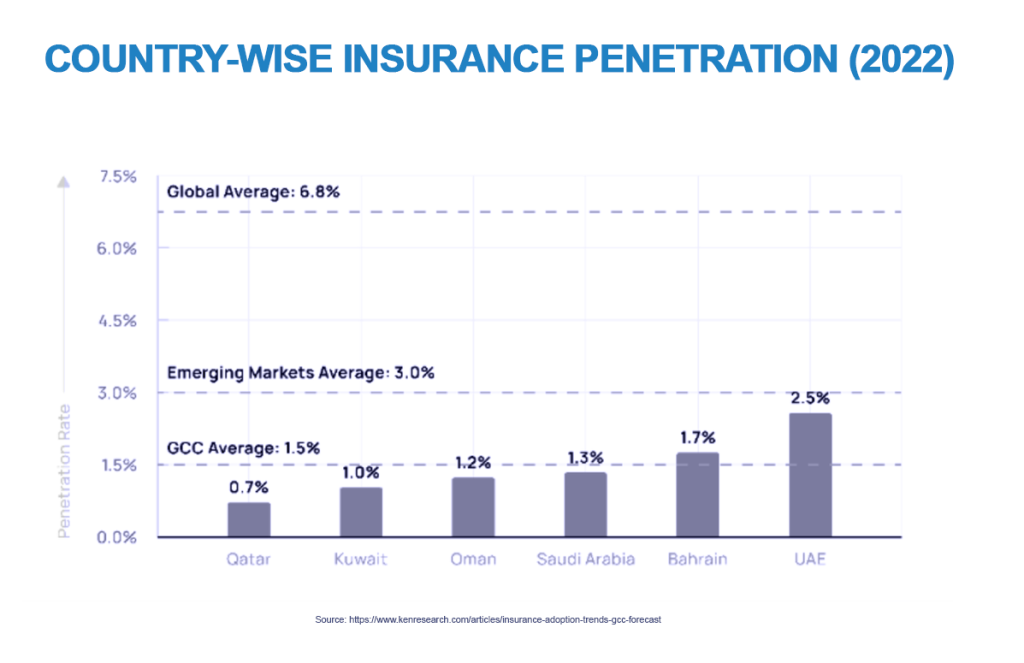

Although stubbornly low insurance penetration rates persist in some Middle East and North African (MENA) markets, gross written premiums (GWP) are expected to grow in the GCC at a CAGR of over 5% by 2028, while North African countries such as Morocco saw GWP growth of more than 5% in 2025[1]. North Africa currently accounts for around 15% of the continent’s total GWP, with Morocco leading the way at around 4%. However, across the GCC, penetration sits below 2% in all member nations except the UAE.[2] Nevertheless, the relatively recent introduction of mandatory cover in motor and/or health lines across many GCC jurisdictions and certain parts of North Africa, including Morocco, Algeria and Egypt, has demonstrated that the policy can contribute significantly to greater penetration.

As a result of this success, several regulatory initiatives to expand compulsory lines, such as employee benefits and unemployment insurance programmes[3] across the region, are promising to deliver greater insurance penetration as governments look to promote further economic stimulus, better social protection and greater risk management among businesses and populations. After all, compulsory lines create immediate demand, especially in markets characterised by poor consumer awareness and relatively low levels of financial literacy, whilst also improving awareness through the widespread acceptance and normalisation of insurance products across entire populations.

How successful are compulsory motor and health lines?

Motor and health now account for the vast majority of non-life premiums, which in turn account for almost 90% of total GCC premiums.[4] Motor is still the largest contributor to the non-life segment through compulsory third-party liability insurance in Morocco, Algeria, Egypt, the UAE, Saudi Arabia and across the GCC, but more recent regulations governing mandatory health cover and employee protection for native and expat populations have contributed to growth in accident and health in recent years, with compulsory health-cover mandates offering the potential to add up to US$ 10 billion in GWP.[5]

Mandatory health cover is beginning to expand and deepen across the region, with a growing number of jurisdictions, including Saudi Arabia, the UAE, Qatar and Kuwait, expanding the scope and depth of health cover mandates through employer schemes for foreign workers and their dependants. Last year, Morocco introduced reforms to its compulsory health insurance to expand beneficiary coverage and give further clarity to eligibility criteria, [6]whilst GCC nations such as the UAE and Saudi Arabia are expanding health coverage beyond native and expat populations to include visitor health cover as tourism continues to grow across the Gulf region. For example, Qatar began the first phase of its compulsory health cover for tourists and visitors in 2023, and other GCC nations such as Bahrain and Oman are following the lead of Saudi Arabia and the UAE in expanding health-cover mandates for expats working in the private sector.[7]

The JENOA view: can the expansion of mandatory cover into nat-cat, property and cyber lines drive further penetration in retail and commercial markets?

To continue building on the success of compulsory cover across the region, governments and regulators have the opportunity to introduce further initiatives to promote greater insurance penetration by expanding, broadening and deepening mandatory lines to cover more economic activity and social protection, whilst promoting greater risk awareness among the wider consumer and commercial markets.

How is natural catastrophe cover linked with property and personal injury?

Residential property insurance remains low in the UAE and wider MENA region, with as few as 15% of homeowners taking out insurance,[8] leaving the majority exposed to risk. As in many other jurisdictions around the world, only property secured against a mortgage or loan in the region requires building insurance and life insurance for the borrower. However, with growing climate risk and natural catastrophes on the rise against a backdrop of rapid urbanisation, protecting populations against the rising costs of repair or rebuilding in the face of fire, floods or other natural catastrophes suggests an element of compulsion in the future.

Oman’s recent mandate for natural catastrophe cover in third-party motor policies[9] underscores the need for insurance cover against extreme weather events and earthquakes across every sector of the economy. Algeria requires compulsory property insurance against natural disasters,[10] and Morocco has led the way in the region with its natural catastrophe protection fund for property and injury. Although this public/private partnership does not require households to purchase natural catastrophe cover directly from insurance providers, all households are automatically opted into the scheme. Households are therefore protected through a combination of a compulsory extension of guarantees against catastrophe risk on the 5% of households that take out private property cover, and a public Solidarity Fund that protects the vast majority of the country’s households that do not enjoy private cover. That Solidarity Fund receives approximately US$ 25 million per annum from a compulsory parafiscal tax on non-life insurance policies, and the resulting accumulation of reserves thus allows the fund to buy cover for excess losses.

Should cyber cover be mandatory for businesses?

Although cyber cover is not yet mandated for all commercial operations in the GCC, certain regulated businesses in the financial services sector are required to have cyber cover in place in Bahrain, the UAE and Saudi Arabia as part of their licensing criteria. Nevertheless, strict data-protection and data-breach reporting rules in many GCC and North African jurisdictions make cyber cover all but mandatory in practice, given the need to mitigate the risk of substantial penalties for non-compliance and liabilities arising from an attack.

In Morocco, mandatory reporting of cyber incidents, especially involving critical infrastructure, was introduced as part of the country’s 2023 National Directive on Information System Security (NDISS),[11] and although compulsory cover is not yet a feature of the regulatory landscape in Morrocco or other north-African nations, the requirement for comprehensive risk management and risk transfer suggests the direction of travel is towards a scenario in which the ongoing resilience of an organisation makes cyber cover all but mandatory.

As governments and regulators implement measures to protect their economies, regulatory authorities may broaden and deepen their reach into sectors of the economy that ignore cyberattack risks. After all, Morocco’s SMEs, for example, are the country’s largest employers, making up around 95% of its private sector[12] and 40% of its GDP,[13] but the protection gaps created by a lack of cover are thought to be significant. Indeed, protection gaps in the region are not limited to North Africa – around 45% of SMEs in the GCC lack any form of cyber cover. This remains a concern for many GCC nations, given that SMEs in the UAE, for example, contribute more than 60% of the country’s non-oil GDP.[14]

What does this mean for MENA clients and how can JENOA help?

JENOA has experience helping the re-insurance industry design tailored solutions for underserved and underinsured markets. With access to the Lloyd’s of London market and major international re-insurance hubs, JENOA leverages conventional Lloyd’s capabilities and global re-insurance expertise. This experience helps authorities and re-insurers establish and promote viable propositions for affordable mandatory lines with increased risk pools to help normalise insurance in jurisdictions with traditionally low penetration rates.

Will we see bigger risk pools and more affordable premiums?

The GCC’s population is forecast to rise to over 80 million by 2050[15] and, as Ken Research notes, “mandatory coverage and demographic expansion will remain the core engines of growth, [with] health, motor, visitor health, and workforce protection schemes [accounting] for most of the GCC’s premium additions”.[16]

However, governments and regulators across the MENA region have the opportunity to build on the recent success of mandatory motor and health cover to protect national populations and their wider economies through an expansion of well-designed and enforced mandatory lines, which in turn will offer consumers and businesses bigger risk pools and more affordable premiums, whilst simultaneously supporting the region’s ambitious growth plans.

DISCLAIMER

This publication is provided by JENOA Ltd. and JENOA Risk Management Ltd. (collectively, “JENOA”) for general informational purposes only and does not constitute legal, regulatory, tax, financial or professional advice. The information contained herein should not be relied upon as a substitute for specific advice from qualified professionals in the relevant jurisdiction.

Regulatory and Legal Information: References to insurance regulations, mandatory coverage requirements, and compliance obligations in any jurisdiction are provided for informational purposes only and may not reflect the most current legal or regulatory developments. Readers should consult with local legal counsel and regulatory authorities to verify applicable requirements before making any compliance or business decisions.

Forward-Looking Statements: This publication contains forward-looking statements regarding potential regulatory developments, market trends, and industry projections. Such statements are based on current expectations and assumptions that are subject to risks and uncertainties. Actual outcomes may differ materially from those expressed or implied. JENOA undertakes no obligation to update forward-looking statements to reflect subsequent events or circumstances.

Limitation of Liability: To the fullest extent permitted by applicable law, JENOA disclaims all liability for any loss, damage, cost, or expense (whether direct, indirect, consequential, or otherwise) arising from or in connection with reliance on any information contained in this publication.

© JENOA Ltd. and JENOA Risk Management Ltd. All rights reserved.

[1] https://www.meinsurancereview.com/Magazine/ReadMagazineArticle

[2] https://www.kenresearch.com/articles/insurance-adoption-trends-gcc-forecast

[3] https://www.kenresearch.com/articles/insurance-adoption-trends-gcc-forecast

[4] https://www.kenresearch.com/articles/insurance-adoption-trends-gcc-forecast

[5] https://www.rgare.com/knowledge-center/article/new-year-to-showcase-the-middle-east-as-an-insurance-market-on-the-move

[6] https://tataachi.com/morocco-reforms-compulsory-health-insurance-2025/#:~:text=Morocco%20Approves%20Landmark%20Reform%20to,more%20efficient%2C%20inclusive%20healthcare%20system

[7] https://www.kenresearch.com/articles/insurance-adoption-trends-gcc-forecast

[8] https://www.insurancebusinessmag.com/asia/news/catastrophe/urgent-call-for-home-insurance-in-uae-following-devastating-dubai-floods-486028.aspx#:~:text=been%20fully%20assessed-,Catastrophe%20&%20Flood,at%20Yallacompare%2C%20discussed%20the%20situation

[9] https://www.reinsurancene.ws/oman-re-and-gallagher-re-support-new-mandatory-nat-cat-cover-for-motor-insurance/

[10] https://www.globaldata.com/store/report/algeria-insurance-industry-government-regulation-analysis/

[11] https://digitalpolicyalert.org/event/25067-implemented-national-directive-on-information-system-security-version-no-22023-establishing-mandatory-security-measures-for-operators-of-cii

[12] https://www.moroccoworldnews.com/2025/01/165781/tax-revenues-and-the-role-of-smes-in-moroccos-economic-transition/#:~:text=In%202023%2C%20Morocco’s%20entrepreneurial%20ecosystem,real%20estate%2C%20and%20professional%20services

[13] https://fsdafrica.org/moroccos-ministry-of-economy-and-finance-launches-new-study/#:~:text=Morocco’s%20Ministry%20of%20Economy%20and%20Finance%20launches,or%20through%20subcontracting%20to%20large%20enterprises%20(LEs)

[14] https://u.ae/en/information-and-services/business/small-and-medium-enterprises

[15] https://qazinform.com/news/un-projects-gcc-population-to-hit-836mn-by-2050-545173

[16] https://www.kenresearch.com/articles/insurance-adoption-trends-gcc-forecast