For insurers, volatility, uncertainty, complexity and ambiguity (VUCA) have long been at the heart of pricing risk; there would be little need for insurance without volatility and uncertainty, and risk managers would be few and far between if we lived in a world without complexity or ambiguity.

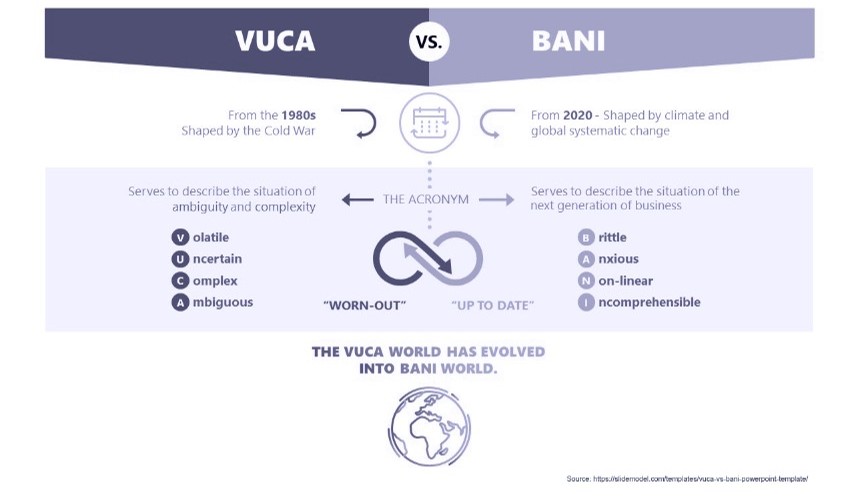

Common in the business lexicon for the last 25 years, the term VUCA originally emerged after the end of the Cold War, when the US Army War College encouraged America’s future generals to consider the complex and multi-faceted global effects of the fall of the USSR. In doing so, they introduced them to the concept of VUCA (volatility, uncertainty, complexity and ambiguity), based on the leadership theories of two pioneering American academics.[1] In other words, it provided a shortcut to understanding how things might pan out and what to expect in a new world order brought about by the demise of the Soviet Union.

Coinciding with the rapid spread of internet use in the early 2000s, the term quickly became synonymous with the challenges facing a global economy struggling to make sense of the sheer speed of technological advancement, change and adoption.[2] For insurers and reinsurers, the risk inherent in those four words – volatility, uncertainty, complexity and ambiguity – has not been entirely without its benefits; uncertainty can spawn new markets and products, and an enhanced appreciation of a company’s increased exposure to risk can often be offset with extended cover to address economic, operational, political or industry risk.

What does VUCA mean for digital insurers in MENA & beyond?

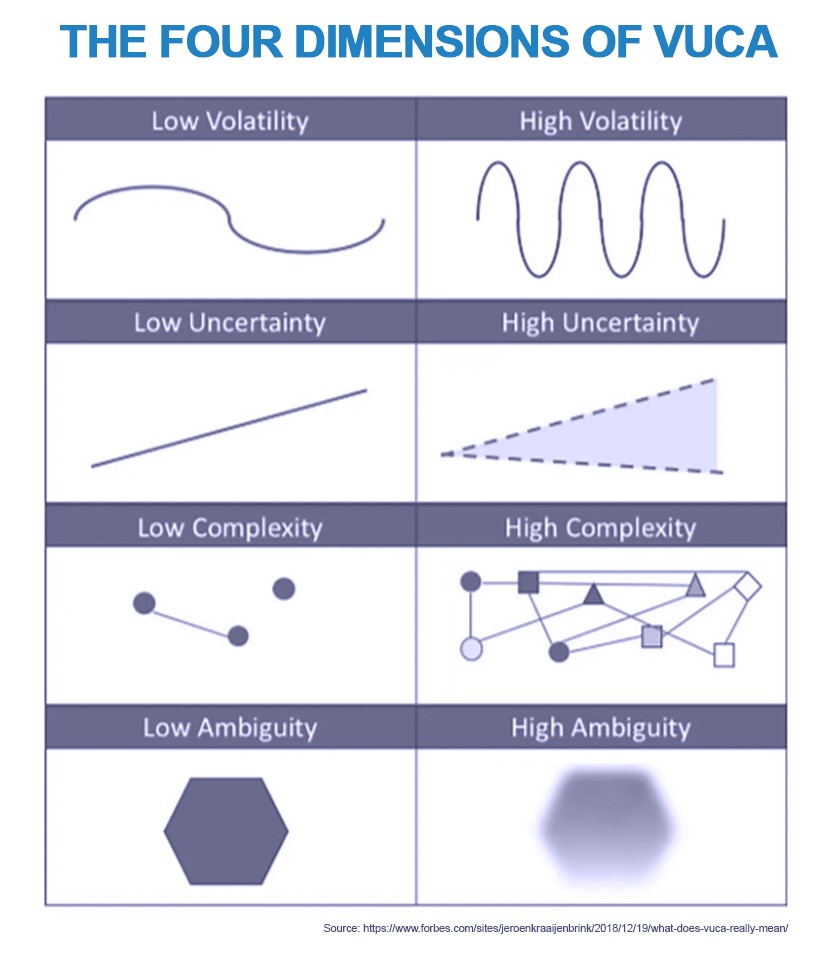

In what Deloitte refers to as “a trendy managerial acronym that conflates the reality of the business environment and the challenges of risk management”, medium- to long-term business plans and objectives can be destabilised without warning by the unpredictable speed of change. The notion of volatility within industries, markets or geopolitics rests on the intensity of fluctuation over time. The greater the volatility or fluctuation, the harder it is for businesses to adapt or pivot in response. Recent disruption to the world’s just-in-time supply chain provides a good example; the confluence of the COVID-19 pandemic, current geopolitical conflict zones and the week-long blocking of the Suez Canal in March 2021, which affected more than 300 vessels, brought unpredictable commodity shortages and wreaked havoc with global supply chains[3].

What characterises the element of uncertainty in the VUCA acronym are its simultaneously subjective and objective natures. While true uncertainty defies the future’s predictability by any statistical measure, uncertainty is also driven, on a subjective level, by people being unable to understand the cause and effect of events, even when the basic characteristics of those causes and effects are known. The more surprises there are, the more unpredictable and uncertain the world becomes.

Deloitte describes complexity as “situations flooded with interconnected variables”. In other words, an overwhelming number of influencing, interconnected and interdependent factors. The more interdependencies and interactions contained in global systems, the greater their complexity, and the harder it becomes to analyse or understand them. Paradoxically, that complexity is heightened by the fact that complex systems cannot, by their very nature, be tinkered with and simplified; they can only be destroyed.

Contradictory, inaccurate or inconclusive information characterised by numerous unknowns with unclear interdependencies creates ambiguity, making it infinitely more difficult to arrive at a conclusion or agree on a particular course of action or mitigation.

From VUCA to BANI

While it is never advisable to allow a corporate understanding of complex, multi-faceted and interconnected global issues to be guided exclusively by simplistic acronyms, these can nevertheless provide a basic framework or checklist from which to plan, navigate and manage risk within an organisation, as well as update and modernise risk-management activities. More recently, the term VUCA has, in the eyes of many, become obsolete[4]. In its place, a new acronym has emerged that underscores a global move from uncertainly to outright instability: BANI.

What does it stand for? The acronym spells out a fragile world that has become brittle, anxious, non-linear and incomprehensible (BANI). The brainchild of American anthropologist Jamais Cascio[5], the term describes a brittleness or fragility that means businesses still clinging to the notion that what worked for them before will always work for them can disappear in the blink of an eye. In short, it underscores the idea that the world is constantly exposed to the risk of catastrophe and, as Cascio claims, it can be “difficult to see the big picture when everyone insists on colouring outside the lines”.

For businesses, anxiety and instability tend to create a sense of urgency that can corrupt good decision-making and undermine an organisation’s ability to make decisions that are robust against uncertainty and ignorance.

Long-term planning is made difficult in a non-linear world because events that seem disconnected can often defy attempts to create well-structured companies; the cause-effect relationship becomes opaque. Standardised corporate structures are ill-equipped to deal with instability and chaos, hampering an organisation’s ability to respond effectively to a rapidly changing business environment for which there has been no rehearsal. However, as widely reported elsewhere[6], the notion of non-linearity is nothing new; non-linearity, or the illusion of predictability, is a common feature of complex global systems.

Does this illusion of predictability and incomprehensible element of BANI mean that businesses must simply accept and face up to the fact that there are very few things that humans can control? Does the illusion of control embodied in BANI’s anxiety say more about people today than about the world?

The JENOA view: risk and opportunity

In spite of all this, as Cascio himself states, “at least at a surface level, the components of the acronym might even hint at opportunities for response”. Brittle systems should be designed with more flexibility; corporate structures could be more poised and responsive to events that do not follow a sequential linear pattern; the decision-making process can be honed by harnessing technology and digitalisation to cut out the superfluous noise around information crucial to a company’s success and survival.

In many respects, the nature of the hazards and risk that businesses in the GCC, MENA and beyond face becomes secondary to the overriding importance of gaining a deeper understanding of exposure and vulnerability. For example, when we consider extreme weather events or natural catastrophes, the number of events and their relative severity often get all the attention from insurers and reinsurers, with less focus on studying vulnerability and understanding society’s exposure.[7]

In a world dominated by unpredictability and instability, as both the VUCA and BANI theories posit, then insurers’ knowledge of future hazards is, by definition, limited. As one long-term expert collaborator with the reinsurance industry notes, “No one can tell you where next year’s hurricanes will hit. However, our knowledge of exposure and vulnerability is limited only by our willingness to expend the resources necessary to measure them”.

Whilst the absence of clarity on available information makes it hard for businesses to interpret it correctly, the transition from a VUCA to a BANI world presents an opportunity for the most agile and innovative insurers. Being able to transform and continuously adapt in a digital world will be key to responding to volatility, uncertainty and instability in the global economy, with insurance cover that can better quantify and price risk through digitalisation while providing clients with the confidence that uncertainty does not have to be an existential issue.

Although there are genuine unknowns that neither insurers nor reinsurers can predict or quantify, harnessing the power of big-data analytics and artificial intelligence (AI) will give digital players a distinct advantage. After all, insurers that fully embrace visibility through digitalisation will be more likely to uncover and mitigate hidden risk in existing systems.

Implications for MENA clients: How JENOA can help

JENOA can support clients in the design of new revenue streams in developing markets in MENA and emerging markets beyond the region, especially where economic or operational instability and uncertainty open up new avenues for responsive digital-product development. JENOA offers a wealth of experience and expertise helping insurance and reinsurance clients in the MENA region adapt to disruption caused by market volatility. As such, we can guide clients towards building structural resilience that is likely to make organisations more resistant to fundamental ignorance and uncertainty.

With access to the Lloyd’s of London market and reinsurance hubs worldwide, JENOA leverages global insurance innovation in tandem with reinsurance capacity to uncover hidden risk and mitigate disruption from VUCA or BANI models with strategic advice to clients.

Adjusting to changing environments

Unbending and brittle corporate-planning structures are not compatible with a non-linear business environment, and businesses that survive will likely be the ones best positioned to react and adapt to changing economic conditions and fast-evolving commercial environments. Companies that do not innovate, and instead fall back on tried and tested methods, will be outstripped by the competition if they do not adjust rapidly to changes in the global marketplace.

[1] https://www.vuca-world.org/where-does-the-term-vuca-come-from/

[2] https://www2.deloitte.com/kh/en/pages/risk/articles/risk-management-in-vuca-environment.html

[3] https://www.bts.gov/data-spotlight/ever-given-suez-canal#:~:text=This%20interruption%20exacerbates%20a%20global,to%20more%20than%20300%20ships

[4] https://hagergroup.com/en/blog/trends-innovation/vuca-bani

[5] https://www.santanderopenacademy.com/en/blog/bani-world.html

[6] https://www.forbes.com/sites/jeroenkraaijenbrink/2022/06/22/what-bani-really-means-and-how-it-corrects-your-world-view/

[7] https://rogerpielkejr.substack.com/p/five-things-everyone-in-reinsurance