With lower-than-average insured losses from natural catastrophes, last year saw a drop of around 25% compared to 2024’s US$ 140 billion[1]. However, 2025 results are only marginally below the ten-year average,[2] and given the volatility of natural catastrophe frequency, the recent softening of the so-called ‘nat-cat’ market reflects competition and over-capacity[3] rather than any dramatic improvement in the risks associated with natural catastrophes and extreme weather.

Natural catastrophes are, by definition, unpredictable, and there remains no compelling upward trend in total annual US losses as a share of GDP. This is largely because insured losses are typically driven by unpredictable catastrophic events, leading to substantial year-to-year variation. As political economist and author Blair Fix notes, “the average severity of big natural disasters is essentially unpredictable – it’s a game of roulette played between humans and the gods of weather”.[4]

As the world continues to place more human and economic assets in harm’s way, adaptation to risk from earthquakes, tropical cyclones, flooding, extreme winds and high atmospheric temperatures, for example, is beginning to make those assets more resilient. This, in turn, has helped curtail catastrophic insured losses, but as the world continues to adapt to a changing climate, whether from anthropogenic influences or through natural variability, further long-term softening of the market due to the current over-capacity of alternative capital is hard to predict, especially against the backdrop of a re-insurance industry grappling with the inherent volatility in the frequency and cost of natural catastrophes.

So what’s causing the softening market?

The 2025 re-insurance losses from natural catastrophes exceeded US$ 100 billion for the sixth year in a row,[5] but at an estimated US$ 107 billion, the total is 24% lower than the US$ 141 billion seen in 2024, and 3% below the 10-year average of US$ 111 billion, according to Swiss Re Institute.

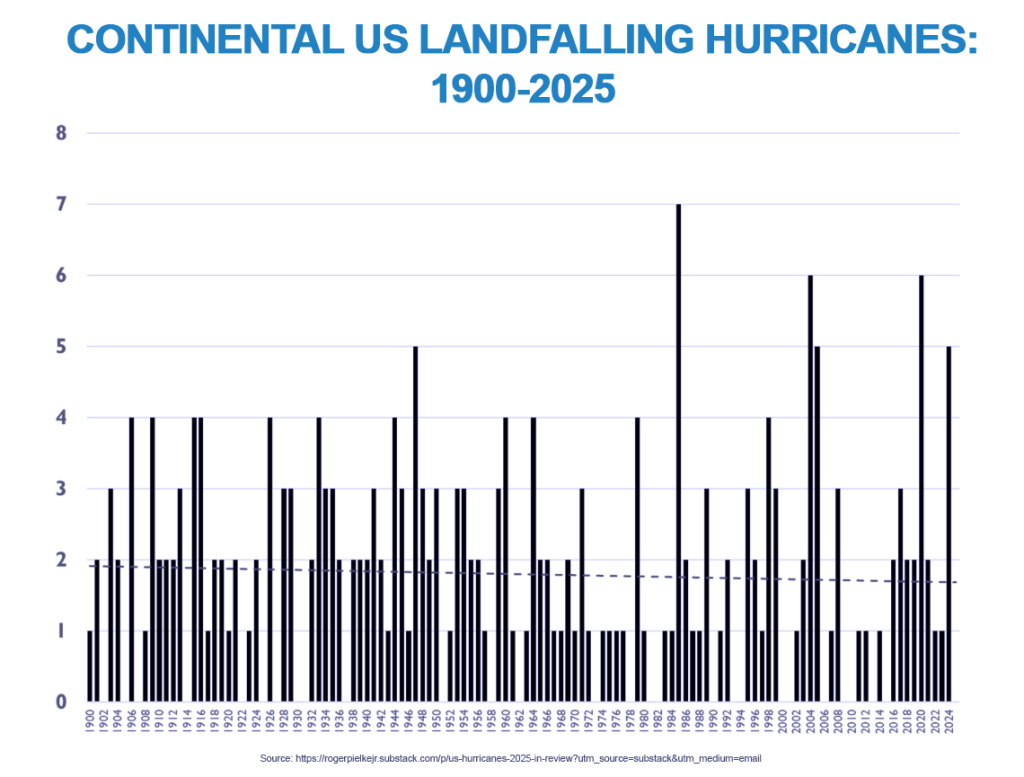

Despite consistent losses, January 2026 renewals saw further drops after two years of declining prices, in part due to the absence of landfalling hurricanes on the US mainland in 2025.[6] After a period of hard market conditions, the nat-cat market began to soften in late 2024 and early 2025. Despite terms and conditions remaining firm, a combination of strong re-insurance returns, over-capacity in capital and the resulting strong competition from alternative-market capacity all appear to have more to do with the softening market than any sudden improvement in the volatility or extremity of natural catastrophes. As J. P. Morgan notes, “price softening continued with April and mid-year renewals marked by a roughly 5-15% decline in rates… Although upper layers of reinsurance programs should become more competitive, driven by the buildup of capital (from both robust returns at existing carriers and increased ILS issuance), the market has not gotten overly aggressive thus far.”

According to the United Nations Office for Disaster Risk Reduction (UNDRR), increasing insurance penetration in a mature US market has helped close the global protection gap. In 2025, that gap fell to a record low of 38%, and shows a vast improvement on the 21st-Century average of 69%. When we consider that the vast majority of 2025 losses were accounted for in the US, we are now in a situation in which the majority of weather-related losses are borne by re-insurers instead of national governments, businesses or individuals. This, in turn, underlines the importance of the re-insurance industry in protecting the global population from the economic losses of natural catastrophes, but also demonstrates that considerable gaps exist elsewhere in the world outside of the developed economies.

The JENOA view: Can we better identify the causes of nat-cat insured losses?

Given that the US accounts for a sizeable majority of global insured losses, and that tropical cyclones have historically accounted for a large proportion of US insured losses, trying to identify any trends in the frequency and strength of land-falling hurricanes on the US mainland is a good place to start. Those trends and their accompanying losses, however, must be seen in the context of modern investment patterns, coastal development and a growing economy.

In 2024, land-falling hurricanes incurred US$ 47 billion in insured losses.[7] Yet, in 2025, the US experienced its first year in a decade without a landfalling major hurricane on the US mainland, underscoring the unpredictability and volatility of natural catastrophes over short timescales. Despite the absence of hurricanes, the US nevertheless accounted for over 80% of global insured, losses[8] driven primarily, according to Swiss Re, by insured wildfire losses of around US$ 40 billion.[9]

The re-insurance industry, however, experienced as it is in adequately pricing risk, is likely to take a more sanguine view when it comes to analysing economic data versus climate and weather data. Disasters occur when natural catastrophes and extreme weather interact with society. Therefore, to detect trends in extreme weather and climate change, it is necessary to examine climate and weather data rather than economic data. By the same token, to better understand or detect trends in natural-catastrophe losses, it appears axiomatic that risk assessment must account for changes in the vulnerability, exposure, and value of human and economic assets to those disasters. For example, as real estate continues to attract investment worldwide as investors search for enhanced returns, the price of real estate has risen faster than income, meaning that as both property values and inflation rise, so too does the economic cost of natural catastrophes.[10] What is certain is that economic loss data, in isolation, tells us less about trends in natural catastrophes than it does about modern developed economies and demographics. An once again, as political economist Blair Fix notes, “the rising frequency of [costly] natural disasters could be an artefact of modern investment patterns.”

Indeed, as Swiss Re points out, “economic development continues to be the main driver of the rise in insured losses resulting from floods, but also other perils, seen over many decades. However, with natural catastrophe risks rising and higher price levels, the annual increase of 5–7% in insured losses will continue, and protection gaps could remain high.”[11][12]

As the United Nations Office for Disaster Risk Reduction (UNDRR) notes, the volatility of natural catastrophes means that when land-falling hurricanes fail to occur, as in 2025, a new risk often takes its place. In the US, for example, wildfire risk has recently been exacerbated not simply by rising real estate values and inflation, but also by expanding settlement patterns as well as longer fire seasons. As mentioned above, Swiss Re underlines this point when it notes that, “2025 produced the highest insured wildfire losses on record (US$ 40 billion). The scale of destruction reflects a convergence of meteorological drivers, such as extended hot, dry conditions and strong winds, with greater exposure – especially housing and high-value residential assets expanding into hazardous wildland-urban interface (WUI) zones.”

What does this mean for MENA clients & how can JENOA help?

With access to global re-insurance markets, including Lloyd’s of London, JENOA’s strong focus on data-driven insights enables us to guide clients toward enhanced analysis of risk exposure, thereby improving underwriting margins and managing natural catastrophe risk more effectively.

When it comes to nat-cat re-insurance, JENOA is well placed in a competitive market to help clients source adequate and suitable re-insurance capacity, as well as help clients innovate to develop new nat-cat-related products using parametric and alternative risk-transfer models.

Can we price risk & reduce losses in a dance between us & the gods of weather?

Firmer terms and conditions, along with further adaptation to promote greater resilience, have the potential to help stem runaway nat-cat losses in the years and decades to come, but the recent softening of the market has little to do with any changes in the nature or predictability of risk posed by global natural catastrophes. As Swiss Re’s Group Chief Economist points out, “amid annual volatility, insured losses keep rising. That’s why strengthening prevention, protection and preparedness is essential to protect lives and property. Reinsurers and the broader insurance sector have a dual role: acting as financial shock absorbers and supporting the development of resilient, risk-informed public policy and private investment that reduce future losses.”

In other words, financial resilience is best advanced through a combination of adaptation and adequate cover.

[1] https://www.reinsurancene.ws/2025-insured-nat-cat-losses-to-exceed-100bn-but-down-24-year-on-year-swiss-re/

[2] https://www.reinsurancene.ws/2025-insured-nat-cat-losses-to-exceed-100bn-but-down-24-year-on-year-swiss-re/

[3] https://www.artemis.bm/news/barring-outsized-cat-losses-reinsurance-pricing-likely-to-get-progressively-softer-j-p-morgan/#:~:text=%E2%80%9CAfter%20more%20than%20a%20decade,increased%20capital%20in%20the%20market

[4] https://economicsfromthetopdown.com/2025/10/26/roger-pielke-jr-s-appallingly-bad-analysis-of-billion-dollar-disasters/

[5] https://www.reinsurancene.ws/2025-insured-nat-cat-losses-to-exceed-100bn-but-down-24-year-on-year-swiss-re/

[6] https://rogerpielkejr.substack.com/p/us-hurricanes-2025-in-review

[7] https://www.munichre.com/en/company/media-relations/media-information-and-corporate-news/media-information/2025/natural-disaster-figures-2024.html#:~:text=In%202024%2C%20tropical%20cyclones%20alone,US%24%2047bn%20were%20insured

[8] https://www.swissre.com/press-release/2025-marks-sixth-year-insured-natural-catastrophe-losses-exceed-USD-100-billion-finds-Swiss-Re-Institute/f710c271-58c8-4c48-9004-05203634d1e0

[9] https://www.swissre.com/press-release/2025-marks-sixth-year-insured-natural-catastrophe-losses-exceed-USD-100-billion-finds-Swiss-Re-Institute/f710c271-58c8-4c48-9004-05203634d1e0

[10] https://economicsfromthetopdown.com/2025/10/26/roger-pielke-jr-s-appallingly-bad-analysis-of-billion-dollar-disasters/

[11] https://www.swissre.com/press-release/Hurricanes-severe-thunderstorms-and-floods-drive-insured-losses-above-USD-100-billion-for-5th-consecutive-year-says-Swiss-Re-Institute/f8424512-e46b-4db7-a1b1-ad6034306352

[12] https://rogerpielkejr.substack.com/p/climate-change-is-showing-its-claws